On April 15, 2015, David Stockman writes on Contra Corner:

Another day of “incoming data” and still more evidence that this isn’t your father’s business cycle. This time it comes from the Eccles Building itself, but don’t expect the Keynesian money printers domiciled there to recognize that the industrial production report they issued today constitutes yet another rebuke to their entire macro model.

The March index slipped badly (0.6%) and thereby predictably elicited a “do not be troubled” assurance from the talking heads. It was just aberrant weather again. Well, that’s actually right. March was so much warmer than February that the utility component of the index plunged by 5.9%.

Indeed, as another branch of the Fed revealed a few days ago, March was actually warmer than normal for the month. Presumably this means the punk economic data for March can’t be explained by winterish weather—-since it is the very opposite condition which explains last month’s steep drop in utility production.

So the better part of wisdom would be to keep the weather and its unpredictable impact on monthly power plant demand out of it. And, as it happens, the trends in the other two components of the index—–mining and manufacturing—-do offer some very pertinent clues about the dismal state of the US economy.

In a word, both of these indices are rolling over on a short-term basis and reflect trend lines which implicate the destructive doings of bubble finance, not the Fed’s pretension that it is rejuvenating the main street economy.

In the case of mining, the March index was down 4% from its December level, yet the decline in actual shale patch output has not yet even started. The recent rollover in the index is mainly attributable to the plunge in coal production, which is now down 20% from it peak three years ago.

In sum, the 30% gain in mining production since the pre-crisis peak is all in the rearview mirror. Mining accounts for about one-seventh of the industrial production index, and, as George W. Bush once said in another context, this sucker is going down.

![]()

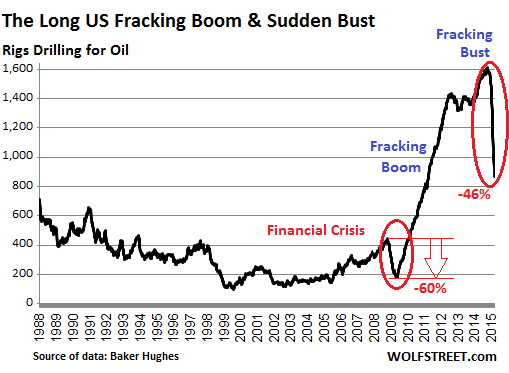

In fact, buried in the mining index is the true handiwork of the global convoy of money printing central banks—-that is, the U.S. crude oil production subcomponent. The People’s Printing Press of China stimulated the greatest construction and industrial boom in recorded history, thereby ballooning the demand for crude oil. At the same time, the Fed drove interest rates to the zero bound, thereby touching off a massive scramble for yield among institutional investors and mutual fund chasing homegamers alike.

So taken together——booming global demand reflected in $115 per barrel oil prices and dirt cheap and plentiful junk bonds and related forms of subordinated capital—-the central banks generated a perfect storm of malinvestment. In less than a decade, the oil rig count went from 200 to 1600 and US oil production surged from 5 to 9 million barrels per day.

Accordingly, the Fed’s index of crude oil production soared. At its current level, which is the highest since 1973, it is up 82% from the pre-crisis peak, and a stunning 133% from the bottom in September 2008.

Needless to say, the shale production surge is not a miracle of capitalism; its an aberration of central bank financial repression. Indeed, cheap and plentiful capital is to shale output what green grass is to a goose. That is, it goes from one end to the other in a remarkably short period of time!

![]()

In fact, after two years from completion, production from a typical shale well declines by 80%. So given the record plunge in oil drilling rigs since last October’s 1600 peak, the oil production index is destined for some considerable retracing to the downside in the years just ahead.

In the case of manufacturing output, the index has been slipping for five months now, but the real story is that it had no place to slip from in the first place. At the March value of 103.1, the index is just 2.2% higher than it was seven years ago in November 2007.

So virtually the entire rise in the manufacturing index that has been celebrated month-after-month by the talking heads has been “born again” production. What they have forgotten to mention was that the build-up of excess inventories and unsustainable production during the Greenspan/Bernanke housing bubble was so extreme that production dropped all the way back 1998 levels at the Great Recession’s bottom.

That is a dramatic contrast with past cycles, and underscores how the Fed’s conventional reflation policy has so completely failed. Compared to the 2.2% growth of manufacturing output during the past seven years, the index rose by 12.5% in the comparable period after the 2000 peak; and, more importantly, it rose by 25% during the seven years after the 1981 peak and 33% during the 1990-1997 cycle.

In other words, the current so-called recovery is not even in the same league. The fact that production is now rolling over—–and the internals reviewed below make that abundantly clear—is powerful evidence that the Fed is pushing on a string when it comes to the main street economy.

Consequently, as it foolishly continues to keep interest rates pinned to the zero bound it is only inflating an even more fantastic financial bubble—–the inevitable bursting of which will send the manufacturing index plunging once again.

![]()

Even this picture is too strong. The minor gains from the 2007 top are entirely attributable to autos, defense and metal fabrications—–much of which went into the booming energy patch and related pipelines and support industries. All of these gains are fueled by cheap debt including the subprime lending boom behind autos.

By contrast, the index for non-durable manufactures is still 5.5% below its pre-crisis peak, and has not yet even regained the level it posted in December 1997. Stated differently, a component which accounts for fully one-fifth of the industrial production index has been going nowhere for 18 years.

The same is true of consumer goods production outside of energy, autos and high tech. The index for March was still 11% below the pre-crisis peak, and also below the level first attained in September 1996.

![]()

Even technology oriented sectors are nothing to write home about. The information processing index, which includes computers and related products, is down 3% from December and is essentially flat with its level in late 2007. In fact, after the enormous boom in which output rose by 5X between 1990 and 2007, the index has essentially flat-lined ever since.

![]()

By contrast to the numerous floundering components of the industrial production index reviewed above, there are enormous vulnerabilities among even those sectors which have experienced meaningful gains in recent years. Front and center on that score is the index for defense and space equipment.

As shown below, the Bush/Obama wars resulted in a 75% gain between 2000 and July 2014. But even the defense bonanza has plateaued out—-a victim of war fatigue in the nation and the sequester caps on defense spending that have finally brought the Pentagon’s procurement spree to a halt.

![]()

Finally, since the June 2009 bottom and GM’s quick rinse discharge from the White House bankruptcy/bailout court, motor vehicle production has been a booster rocket. Output has more than doubled from the 2009 bottom.

But even here there is much less than meets the eye. The 50% plunge of the auto production index during the Great Recession was an artifact of Washington’s machinations before and during the financial crisis.

In the first instance, it reflected a massive inventory liquidation on the dealer lots during 2008-2009. Several million excess vehicles needed to be sold-down in order to make room for new production—–a distortion which, in turn, had been fueled by the Wall Street subprime lending boom enabled by the Fed.

On top of that, the complete disruption of production at Chrysler and General Motors owing to the bailouts and bankruptcies during 2009 further depressed production. During most of late 2008 and early 2009, the entire executive leadership of the auto industry was running to Washington rather than running their plants and operations.

So much of the “born again” recovery in auto production shown in the graph below was simply a rebound from the prior Washington orchestrated disruption. Now that inventories have been rebuilt and then some, however, the pace of expansion has sharply slowed.

At the same time, the resurgent sub-prime auto credit boom of the past two years is getting long-in-the-tooth. Delinquency rates on newly issued credits are now rising rapidly, and the issuance rate has flattened out in recent months.

In any event, after soaring by 130% between June 2009 and June 2014, auto production has essentially flat-lined since then. Indeed, with sales at the 17 million mark and the subprime market tapped-out, it is hard to see where any further gains will occur in motor vehicle production.

The more likely direction is down. Indeed, that is a guaranteed outcome when the Wall Street bubble finally bursts. Like last time, it will shatter confidence among the gamblers who essentially fund the purchase of low end vehicles in the subprime market, thereby drying up demand in what amounts to the rent-a-car industry. By the same token, the top 10% of households, which own the stock and buy the luxury end of the auto market, will be sidelined trying to reach their brokers.

![]()

At the end of the day, the meaning of today’s incoming industrial production data is that the Fed has not fueled an industrial recovery in any meaningful sense of the word. Outside of energy and defense, which are reversing, and motor vehicles, which have tapped out the household sector’s remaining credit veins, there have been virtually no industrial production gains at all.

So once again the Fed is pushing on a string and inflating a gargantuan financial bubble. That much is plainly evident in the Fed’s own data releases. Indeed, the real truth is that the Fed’s massive money printing during this entire century—-which has expanded its balance sheet by 9X from $500 billion to $4.5 trillion—-has done nothing for the industrial economy.

As shown below, the March index for production of fabricated metal products posted at 99.2 or almost exactly where it stood in June 2000. During the 15-year interim there was a long-lived, but artificial oil production boom and two auto production cycles—-both of which sectors are heavy users of fabricated metal components. Yet those tailwinds were not enough to lift the index, nor did the Fed’s massive money printing campaigns make any difference.

![]()

Unfortunately, there is no prospect that Janet Yellen and her merry band of money printers will shed their Keynesian blinders at any time soon. So they will dither until the bubble bursts under its own weight and sends the industrial production index into another round of cliff-diving.

Maybe then someone will ask exactly how it is that real production and wealth can come out the end of a printing press. The Fed’s own data series proves overwhelmingly that it doesn’t.