GETTY

On January 15, 2018, Noah Kirsch writes on Forbes:

Wealth concentration in the United States—which is intensifying across the board—has impacted minority groups the hardest.

That is the thesis of a new report from the Institute for Policy Studies, a left-leaning think tank based in Washington, D.C.

Utilizing data from the Federal Reserve, Bureau of Labor Statistics and Forbes rich lists, among other sources, the institute found that the 400 richest Americans hold more wealth than “all Black households, plus a quarter of Latino households [combined].”

Separately, the study noted, “Between 1983 and 2016, the median Black family saw their wealth drop by more than half after adjusting for inflation, compared to a 33% increase for the median White household.” At present, the median Black family has assets of $3,600, roughly 1/4oth that of the median White household, the institute reports.

INSTITUTE FOR POLICY STUDIES

Among the study’s other striking conclusions:

- Black families are about 20 times more likely to have zero or negative assets (indebted) than they are to be worth $1 million or more. Latino households are 14 times more likely to have zero or negative assets than they are to be millionaires. Meanwhile, white households are equally likely to fall into either category.

- The wealth of the median Latino family rose 54% between 1983 and 2016, to $6,600. Still, the wealth of typical Latino household is 1/22nd that of the median white household.

“Wealth is where the past shows up in the present. From slavery to Jim Crow, to redlining, to mass incarceration, the division of assets on the basis of race has been explicit public policy for centuries,” says Josh Hoxie, one of the study’s co-authors.

International disparities resemble those in the United States. Of the 2,043 individuals who made Forbes’ 2018 list of the World’s Billionaires, just 11 were black. Additionally, a 2018 Oxfam analysis found that the world’s 42 richest people hold as much wealth as the poorest 3.7 billion people combined.

The Institute for Policy Studies’ latest report emphasizes that wealth concentration in the U.S. is increasing across demographics. For instance, the three richest Americans—Jeff Bezos, Bill Gates and Warren Buffett—hold more wealth than the bottom 50% of the country combined, the institute says. That statistic mirrors the barrier to entry for The Forbes 400.In 1982, the list’s inaugural year, the minimum net worth was $100 million. This year the cutoff hit an all-time high of $2.1 billion.

Inversely, a 2017 Federal Reserve report found that 40% of adults would not have the cash to cover an unexpected expense of $400. The same report found than one in five adults cannot pay all of their monthly bills, while more than a quarter skip necessary medical care because they can’t afford it.

Some billionaires, including Bill Gates, have acknowledged the significance of wealth and income inequality. “High levels of inequality are a problem—messing up economic incentives, tilting democracies in favor of powerful interests, and undercutting the ideal that all people are created equal,” Gates wrote in a 2014 blog post. His wife, Melinda, echoed the sentiment in their foundation’s 2018 annual letter: “It’s not fair that we have so much wealth when billions of others have so little. And it’s not fair that our wealth opens doors that are closed to most people.”

For his part, Warren Buffett cites “an advanced market-based economy” for the gap between the rich and the poor. Still, he wrote in a 2015 op-ed, “The poor are most definitely not poor because the rich are rich. Nor are the rich undeserving.”

Reversing current trends is proving difficult. Proposals range from establishing bonds for young children, to guaranteeing a basic income, to raising the estate tax, to expanding access to affordable medical care and housing—any of which is guaranteed to be politically explosive. Identifying a problem is often easier than fixing it.

Gary Reber Comments:

The report and the author uses terms as “wealth concentration,” “hold more wealth,” and “has assets of,” which are indirect ways of describing capital asset ownership — the accumulation of such makes people rich or wealthy.

The system has been structured, unnecessarily, to require past savings be pledged to lending institutions to secure capital credit, even with projects formed that generate earnings sufficient to liquidate the capital credit extended to finance growth.

The system must be reformed to empower EVERY child, woman and man to acquire ownership in self-liquidating productive capital asset formation, without the requirement of past savings or any other requirement other than citizenship. Capital credit insurance can replace the past savings requirement. And because there is no need to depend on the past savings of the already wealthy, the capital credit can be interest-free with only the modest cost of loan management.

Productive capital asset formation in which the earnings from the assets formed are expected to generate sufficient earnings to pay off the capital credit is inherently insurable. Note: the mortgage insurance paid by the nation’s acquiring homeowners provides a pool of monies to pay off banks in the event of foreclosure or loss of a home under the insured Federal Housing Administration (FHA) home mortgage acquisition program. Yet a home used to live in does not generate any income for the homeowner and requires a separate source of earnings from which to pay the monthly mortgage (including the approximate 2.5 percent mortgage interest).

Requiring a separate income source is not the case with the formation of new productive capital assets. Capital acquisition takes place on the logic of self-financing and asset-backed credit for productive uses. People invest in capital ownership on the basis that the investment will pay for itself. The basis for the extension of capital credit and commitment of loan guarantees is the fact that nobody who knows what he or she is doing buys a physical capital asset or an interest in one (existing or to be formed) unless he or she is first assured, on the basis of the best advice one can get, that the asset in operation will pay for itself within a reasonable period of time — five to seven or, in a worst case scenario, 10 years (given the current depressive state of the economy). And after it pays for itself within a reasonable capital cost recovery period, it is expected to go on producing income indefinitely with proper maintenance and with restoration in the technical sense through research and development.

Still, there is at least a theoretical chance, and sometimes a very real chance, that the investment might not pay for itself, or it might not pay for itself in the projected time period. So, there is a business risk. To solve the chance of risk, the risk can be absorbed by capital credit insurance or commercial risk insurance. Thus, in order to achieve national economic democracy, we need a way to handle risk management in finance by broadly insuring the risks. Such capital credit insurance would substitute for the security demanded by lenders to cover the risk of non-payment, thus enabling the poor and others with no or few assets (the 99 percent) to overcome the collateralization barrier that excludes the non-halves from access to wealth-creating, income-generating productive capital.

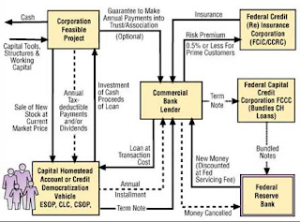

One feasible way to significantly broaden capital ownership simultaneously with the responsible growth of the economy is to lift ownership-concentrating Federal Reserve System credit barriers and other institutional barriers that have historically separated owners from non-owners and link tax and monetary reforms to the goal of expanded capital ownership. Removing barriers that inhibit or prevent ordinary people from purchasing capital that pays for itself out of its own future earnings is paramount as an actionable policy. This can be done under the existing legal powers of each of the 12 Federal Reserve regional banks (Section 13(2)), and will not add to the already unsustainable debt of the federal government or raise taxes on ordinary taxpayers. We need to free the system of dependency on Wall Street and the accumulated savings and money power of the rich and super-rich who control Wall Street. The Federal Reserve System has stifled the growth of America’s productive capacity through its monetary policy by monetizing public-sector growth and mounting federal deficits and “Wall Street” bailouts; by favoring speculation over investment; by shortchanging the capital credit needs of entrepreneurs, inventors, farmers, and workers; by increasing the dependency with usurious consumer credit; and by perpetuating unjust capital credit and ownership barriers between rich Americans and those without savings. The Federal Reserve Bank should be used to provide interest-free capital credit (including only transaction and risk premiums) and monetize each capital formation transaction, determined by the same expertise that determines it today — management and banks — that each transaction is viably feasible so that there is virtually no risk in the Federal Reserve. The first layer of risk would be taken by the commercial credit insurers, backed by a new government corporation — the Capital Diffusion Reinsurance Corporation (CDRC) — through which the loans could be guaranteed. The CDRC would reinsure any portion of any financing risk assessed as reasonable and insurable but not already insured by the commercial capital credit insurance underwriters. In establishing the CDRC, the federal government would not be undertaking a new responsibility but merely simplifying and rationalizing an existing one. This entity would fulfill the government’s responsibility for the health and prosperity of the American economy.

The Capital Diffusion Reinsurance Corporation would function similar to the Federal Housing Administration, generally known as “FHA”, which provides mortgage insurance on loans made by FHA-approved lenders throughout the United States and its territories. The FHAinsures mortgages on single family and multifamily homes including manufactured homes. While pay-downs on home mortgages require a separate source of income, capital credit for productive capital formation is self-liquidating, with the earnings from the investment the source of the pay-down.

This proposal was not mentioned in the article, yet it is the singular proposal that would result in simultaneously creating new productive capital asset owners as the economy expands, without taking from those who already own.

To read more see my article

“Economic Democracy And Binary Economics: Solutions For A Troubled Nation and Economy” at http://www.foreconomicjustice.org/?p=11 and support the enactment of the proposed Capital Homestead Act (aka Economic Democracy Act and Economic Empowerment Act) at http://www.cesj.org/learn/capital-homesteading/, http://www.cesj.org/learn/capital-homesteading/capital-homestead-act-a-plan-for-getting-ownership-income-and-power-to-every-citizen/, http://www.cesj.org/learn/capital-homesteading/capital-homestead-act-summary/ and http://www.cesj.org/learn/capital-homesteading/ch-vehicles/. And The Capital Homestead Act brochure, pdf print version at http://www.cesj.org/wp-content/uploads/2014/11/C-CHAflyer_1018101.pdf and Capital Homestead Accounts (CHAs) at http://www.cesj.org/learn/capital-homesteading/ch-vehicles/capital-homestead-accounts-chas/