On February 12, 2019, Sophie Caronello and Brendan Murray write on Bloomberg:

On February 12, Steve Benen writes on MSNBC:

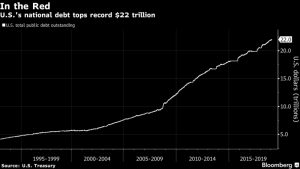

For those concerned with the national debt, yesterday brought some discouraging news: the debt officially topped $22 trillion. The Associated Press reported:

“The Treasury Department’s daily statement showed Tuesday that total outstanding public debt stands at $22.01 trillion. It stood at $19.95 trillion when President Donald Trump took office on Jan. 20, 2017.

The debt figure has been accelerating since the passage of Trump’s $1.5 trillion tax cut in December 2017 and action by Congress last year to increase spending on domestic and military programs.”

It was three years ago last week when Donald Trump appeared on Fox News and assured viewers that, if he were president, he could start paying off the national debt “so easily.” The Republican argued at the time that it would simply be a matter of looking at the country as “a profit-making corporation” instead of “a losing corporation.”

A month later, in March 2016, Trump declared at a debate that he could cut trillions of dollars in spending by eliminating “waste, fraud, and abuse.” Asked for a specific example, he said, “We’re cutting Common Core.” (Common Core is an education curriculum. It costs the federal government almost nothing.)

A month after that, in April 2016, Trump declared that he was confident that he could “get rid of” the entire multi-trillion-dollar debt “fairly quickly.” Pressed to be more specific, the future president replied, “Well, I would say over a period of eight years.”

By July 2016, he boasted that once his economic agenda was in place, “we’ll start paying off that debt like water.”

When making a list of Donald Trump’s most audacious broken promises, this one belongs near the top.

Complicating matters, I’m not altogether sure the president understands what the national debt is or how it changes. Two weeks ago, a reporter asked him why, during a period of economic health, the deficit and debt are growing rapidly. “Well,” Trump responded, “the trade deals won’t kick in for a while.”

There was no meaningful relationship between the question and the answer. The president’s response was effectively gibberish.

It’s possible, of course, that this was Trump’s way of dodging a difficult question about one of his more obvious failures. It’s also possible that he’s genuinely lost and doesn’t know the meaning of some pretty basic terms.

Either way, the debt that Republicans only pretend to care about during Democratic administrations continues to reach new heights – or in this case, depths.

On February 12, 2019, Martin Crutsinger writes on ABC News:

The national debt has passed a new milestone, topping $22 trillion for the first time.

The Treasury Department’s daily statement showed Tuesday that total outstanding public debt stands at $22.01 trillion. It stood at $19.95 trillion when President Donald Trump took office on Jan. 20, 2017.

The debt figure has been accelerating since the passage of Trump’s $1.5 trillion tax cut in December 2017 and action by Congress last year to increase spending on domestic and military programs.

The national debt is the total of the annual budget deficits. The Congressional Budget Office projects that this year’s deficit will be $897 billion — a 15.1 percent increase over last year’s imbalance of $779 billion. In the coming years, the CBO forecasts that the deficit will keep rising, top $1 trillion annually beginning in 2022 and never drop below $1 trillion through 2029. Much of the increase will come from mounting costs to fund Social Security and Medicare as the vast generation of baby boomers continue to retire.

The Trump administration contends that its tax cuts will eventually pay for themselves by generating faster economic growth. That projection is disputed by many economists.

Despite the rising levels of federal debt, many economists say they think the risks remain slight and point to current interest rates, which remain unusually low by historical standards. Still, some budget experts warn that ever-rising federal debt poses substantial risks for the government because it could make it harder to respond to a financial crisis through tax cuts or spending increases.

Michael Peterson, head of the Peter G. Peterson Foundation, says “our growing national debt matters because it threatens the economic future of every American.”

The United States increasingly is supporting its government operations through debt financing, and as a result, the nation’s debt continues to grow. To reverse course and steadily eliminate our national debt and operate with a balanced budget will require system reform and significant growth of the economy, along with the self-financing of FUTURE wealth-creating, income-producing productive capital assets that will create new owners who become “customers with money” to sustain growth.

In the United States, the reform of the financial system that resulted in the National Banking Act of 1863 restricted the non-rich to the existing (and diminishing) pool of past savings to finance new capital formation and economic development, while the rich could create their own money for the same purpose by issuing bills of exchange. The National Banks and state banks functioned as banks of deposit for the non-rich, severely restricting participation in the economic common good, while they served as banks of issue for the rich, giving them a virtual monopoly over the ownership of new productive capital assets other than homestead land and small ancillary businesses.

Unfortunately, both capitalism and socialism rely on the demonstrably false premise that the only way to finance new productive capital formation is to cut consumption and accumulate money savings; financing for all new productive capital is presumed to come out of the present value of production that was withheld from consumption.

As Harold Moulton demonstrated in The Formation of Capital (1935), reducing consumption (withholding production from consumption) in order to finance new capital formation harms the financial feasibility of the new productive capital the investor intends to finance. It can even, when the investor realizes that there is insufficient consumer demand to justify the new productive capital formation, prevent the new productive capital from being formed in the first place.

Given that, as Adam Smith said, the sole purpose of production is consumption, one can reasonably conclude that it is contrary to the purpose of production to withhold production from consumption in order to finance new productive capital to increase production. More simply put, if we are not consuming all that is being produced now, of what conceivable use is it to increase production?

That is the “economic dilemma” (as Moulton put it) facing the “capitalist,” or (in socialism) the State if it takes over control of the economy. It should be obvious that new productive capital investment must take place if economic activity is to be sustained. At the same time, the individual investor cannot justify financing the formation of additional new productive capital when there is clearly insufficient demand for what existing productive capital is already producing.

It is, to all appearances, a perfect “Catch 22” situation. If the capitalist invests in new productive capital when there is no demand for what the productive capital will produce, he or she will go bankrupt. If, on the other hand, there is a demand for all that is being produced and more besides, there is little or no possibility of withholding anything from consumption to use in financing new productive capital formation.

Past savings — the present value of past cuts in consumption — are not, however, the only or even the best source of financing for new capital formation. There is also “future savings,” that is, the present value of future increases in production. Just as derivatives (“money”) called mortgages can be created using the present value of existing marketable goods and services as the “underlying” asset backing the derivative, derivatives called bills of exchange can be created using the present value of future marketable products and services as the underlying.

Believing — erroneously — that past savings are the only source for financing of new productive capital formation has one of two results. If we believe that the market will take care of things without the State doing more than policing abuses, enforcing contracts, and in general providing a level playing field, we end up with capitalism. Ownership of productive capital must be concentrated in the hands of a private sector elite, for only people whose productive capital assets produce far more than they can consume can afford to finance the formation of new productive capital, thereby providing jobs for the rest of us, to the extent that they are not necessary due to ever-increasing shifts in the technologies of production.

If, however, we believe that the market and private initiative cannot be trusted to take care of things, and that government action is required to both regulate and control the private sector so that everyone will be taken care of adequately and there will be sufficient investment to create enough jobs (whether or not we believe State control will continue to be necessary, or it will wither away), the State must take an ever-increasing role in the economy. That is socialism.

The way to avoid the fallacies of both capitalism and socialism is to realize that new productive capital formation can be financed better using the present value of future increases in production –– future savings –– than by using the present value of past cuts in consumption –– past savings. Reliance on past savings, however (despite its obvious falsity) is accepted as an absolute dogma by all mainstream schools of economics, and virtually all of their offshoots. That is the challenge –– to re-educate.

Of course to succeed practically in creating broadened private, individual ownership of FUTURE productive capital formation, there must be a provision to secure investment. This is where collateral insurance comes in (i.e. the provision of sufficient security to support a loan for productive capital acquisition). Because beneficiaries would be enabled to undertake financing on the strength of non-recourse pure capital credit loans from banks and other lenders, the question of collateral or other satisfactory security security to support the loans is critical. Banks cannot extend pure capital credit without security to cover the risk of the borrower’s inability to repay the loan. Nor can existing owners be saddled with the risk of business failure. Thus the risk of productive capital investment failure (a risk that is now borne primarily by existing owners, but with considerable governmental back-up mediation through economic intervention by way of taxing, borrowing, monetary, regulatory and other powers) can instead be commercially insured with government reinsurers in reserve if necessary. This would be included as an element in the cost of borrowing in the case of each pure capital credit loan to provide financial compensation to the lenders. Similar insurance mechanisms can be employed as used by the U.S. Federal Housing Administration (FHA) to overcome the formidable financial barrier that prevents most people form effective productive capital acquisition. Once we set put on this path to prosperity, opportunity, and economic justice it is an open question whether government involvement (and how much and in what form) is necessary to promote the market provision of pure capital credit insurance. In the writings of binary economist Louis Kelso, he consistently proposed the creation of an agency to operate on the broad principles as practiced by the FHA in providing loan insurance to home buyers. The FHA has experienced decades of profitable success in facilitating the financing of broader home ownership throughout the United States. Instead of financing with insured loans a consumer purchase (a home to live in) we would be financing productive capital asset formation that generates its own earnings out of which to pay back the loan. Capital credit insurance is not a government guarantee. To the contrary, capital credit insurance would be provided only if the premium is competitively attractive in view of the risk insured. Any investment risk that is not insurable on market principles should not be undertaken. The government’s reinsurance corporation would be expected to meet the profitable performance standards of programs like the FHA’s home loan insurance program.

For more on how to accomplish such structural reform, see “Financing Economic Growth With ‘FUTURE SAVINGS’: Solutions To Protect America From Economic Decline” at http://www.foreconomicjustice.org/?p=17032 and “The Income Solution To Slow Private Sector Job Growth” at http://www.foreconomicjustice.org/?p=9872.

Support the Agenda of The Just Third Way Movement at http://foreconomicjustice.org/?p=5797 and support the Capital Homestead Act (aka Economic Democracy Act and Economic Empowerment Act) at http://www.cesj.org/learn/capital-homesteading/, http://www.cesj.org/learn/capital-homesteading/capital-homestead-act-a-plan-for-getting-ownership-income-and-power-to-every-citizen/, http://www.cesj.org/learn/capital-homesteading/capital-homestead-act-summary/ and http://www.cesj.org/learn/capital-homesteading/ch-vehicles/.