On April 13, 2020, Thomas Wright and Kurt M. Campbell write in The Atlantic:

If Joe Biden wins the election in November, he will likely be sworn in—perhaps virtually—under the most challenging circumstances since Harry Truman became president in 1945. The country will probably be in the end stages of a brutal pandemic and faced with the worst economy since the Great Depression. The Treasury will be significantly depleted. Millions of people will have lost loved ones, their jobs, much of their net worth. Hopefully a vaccine or an effective treatment will be closer to reality, and our national attention can shift to what comes next.

We judge our great presidents by how they managed harrowing trials and wars: Abraham Lincoln and the Civil War; Franklin D. Roosevelt and the Depression, followed by World War II; Ronald Reagan and the Cold War. But many of the bigger and less historically rewarding challenges are what come immediately after—how to rebuild and remake the country and engage in the wider world. Think about Ulysses S. Grant and Reconstruction, Woodrow Wilson and the League of Nations, Truman and the architecture to wage the Cold War, George H. W. Bush and the collapse of the Soviet Union. Some failed; others succeeded. All faced enormous obstacles explaining what just happened, what had changed, and how we must adapt. This is the category of presidency that Biden, or Donald Trump if he is reelected, will find himself in.

If Trump wins, the country can expect more of what we have seen in the initial phase of dealing with COVID-19—shifting the economic and health burden to the states and Congress, a lack of interest in international cooperation, and a refusal to critically scrutinize the response.

But what about Biden? The beginning of his presidency will have a unique logic and character that sets it apart from the early stages of the crisis. His first year will be shaped in various measures by the public reaction to the horrors of 2020, the national Rorschach test of seeing Trump’s silhouette finally from a remove, and a dawning reality of exceedingly difficult choices across the board.

Biden’s first and toughest challenge will be to address the badly frayed governance compact, in which citizens expect and trust the government to deliver on essential services. For decades, Republicans and Democrats have believed that the government needs fixing, albeit for very different reasons. Republicans tend to view much of the state apparatus, including regulatory bodies and social services, as inherently inefficient and run by entrenched, unaccountable bureaucrats. Democrats see our federal workforce as under-resourced and frequently subjected to quixotic and unreasonable demands from political leaders. However, many Americans, particularly those with means, have been shielded from the consequences of a broken government. The economy has generally been good, and the wealthy purchase better education and health care from the private sector.

COVID-19 lays bare the weaknesses of the American system for all to see. It shows that the crisis of governance is much worse than either party believed. And, no one can fully escape the cost. The twist of the knife is that some other democracies performed much better than the United States. Taiwan, South Korea, New Zealand, and Germany were able to test quickly and en masse, and seem poised to convert that into a program of broad public-health surveillance that allows a more targeted approach, which in turn facilitates less draconian economic measures. Or consider the stimulus. Like the United States, the Canadian government also cut its citizens a check. But unlike America, the Canadian checks were directly and automatically deposited into their accounts days later. In America, receiving aid can take months, and only after people navigate an abundance of red tape.

Keeping America safe is supposed to be one of the core competencies of the federal government, whether you are a Republican or a Democrat. Many people feel that is no longer the case. A Biden administration will have to design careful, constructive steps to rebuild public trust even as the reaction to the pandemic will likely continue to cleave blue and red. Urban dwellers, who have so far been the hardest hit by the virus, will be more open to the role of government in trying to patch social services and rebuild pandemic preparedness. Rural residents might be more focused on the economy and less on government safety nets.

Biden’s second herculean task will be resurrecting the national economy. By January 2021, the United States will likely have tried numerous unprecedented fiscal and Fed efforts to keep the faint pulse of the national economy going, but unemployment will still be in the double digits and entire industries will remain decimated. With the end finally in sight, the government will need to urgently figure out how to get as many businesses as possible up and running and people back to work. This effort would be challenging in the best of times, but the pandemic likely will have changed the very nature of work in America. A simple restart is not possible. The rise of telework, the demise of retail, the uncertainties of the gig economy, more automated manufacturing, and even the role of restaurants in this new environment will take time to sort out.

The pandemic is also a vivid reminder that millions of Americans lack basic protections that are taken for granted in other democracies, such as unemployment benefits, sick leave, and health insurance. After the crisis hit, Republicans in Congress worked with the Democratic House to enact many reforms to temporarily fill these gaps for people. Republicans’ ideological flexibility in the age of Trump no doubt helped with their rapid weaving of a safety net, but with Biden at the helm, they will undoubtedly return to their concern about the deficit and spending. The next president must strive to consecrate, continue, and improve this renewal of the social contract, taking lessons not from Western Europe, but from Asia—Taiwan, Singapore, and South Korea—where the most efficient public sectors exist. Biden will also have to urgently repair and improve the Affordable Care Act, which Republicans have tried to dismantle over the past few years.

The third challenge is international. The Trump administration has failed to lead and organize the world in responding to COVID-19. Trump, at times, alienated allies when he enacted uncoordinated travel bans and competed with them for scarce medical resources. This behavior has undoubtedly made the crisis worse, but cooperation will be much more important at the end of the pandemic than it was at the beginning. Right now, all governments are rightly preoccupied with their national crises. But in 2021, a number of crucial problems must be addressed collectively. How can the vaccine be distributed globally, at a reasonable cost, and to those who need it most? How can governments work together to put in place an international architecture of surveillance, rapid response, and a scalable industrial base for crucial medical supplies so everyone is prepared for the next pandemic? As governments rebuild their national economies and focus on restoring their domestic industries, how do they do so in a way that also creates a healthy global economy that works to everyone’s benefit? And, as the world opens back up, how can countries deal with the geopolitical crises that will inevitably emerge from this period?

The Biden administration will need to not only convene the international community but, like Roosevelt, Truman, and Bush, provide a vision for the path forward. This will require equal measures of leadership, humility, flexibility, and determination. Unlike the post–World War II era, when Europe was rubble, Asia chaos, and the American homeland untouched and economy ready to roar, the global recovery is this time likely to be led by Asia, with China ascendant and ambitious. The world will be more multipolar but decidedly Asian-themed.

This leads to the most vexing post-coronavirus challenge: how to manage the China dimension. China’s failure to be honest about COVID-19 increased the risks to the rest of the world, its pressure on the World Health Organization compromised a vital international institution when people needed it most, and its propaganda war to place the blame on the United States amounted to the throwing of a gauntlet in a superpower competition. These outrages are layered upon a mounting strategic rivalry over values and interests that infuses the geopolitics of Asia but is also taking on global dimensions. For instance, China is vigorously pursuing its territorial claims in the South China Sea; using its substantive economic might to coerce countries on a wide range of issues, including the status of Taiwan and human rights; and pushing its Belt and Road Initiative in a way that ignores decades of best practice from the World Bank and other institutions. The task confronting the next administration will be without precedent in our history. The U.S. has had outright enemies before, and also countries with whom it is deeply engaged and intertwined. But these have always been decidedly separate groups.

Trump looks set to oscillate between pressuring China on trade and using hyperbolic rhetoric to blame the country for the virus, and praising Xi Jinping personally and abdicating any leadership role in the competition over values. Biden’s challenge will be to fashion a relationship that does not descend into all-out strategic competition. He will need to marshal a global coalition that presents China with both opportunities and constraints, and will need to provide a compelling vision for how to cooperate on shared problems, like pandemic preparation and climate change. At the same time, the coalition will need to shift necessary military capabilities to the Pacific and redirect national capacities long focused on the Middle East to Asia. The U.S. has gotten a late start and taken several detours on the way to an Asia-centric strategy, but that starts with a vengeance now.

For Biden, his post-pandemic agenda cannot be an exercise in restoration. It will have to be a master class in redesign, a national effort made more difficult by empty coffers, a frayed social safety net, an uncertain economic environment, a populace venturing outside for the first time in many months, and a daunting challenger rising across the Pacific.

Gary Reber Comments:

According to this The Atlantic editorial entitled “If Biden Wins, He’ll Have To Put The World Back Together,” should Joe Biden (or Donald Trump) win the office of the presidency, “Biden’s second herculean task [the first being rebuilding public trust to unite us] will be resurrecting the national economy. By January 2021, the United States will likely have tried numerous unprecedented fiscal and Fed efforts to keep the faint pulse of the national economy going, but unemployment will still be in the double digits and entire industries will remain decimated. With the end finally in sight, the government will need to urgently figure out how to get as many businesses as possible up and running and people back to work. This effort would be challenging in the best of times, but the pandemic likely will have changed the very nature of work in America. A simple restart is not possible. The rise of telework, the demise of retail, the uncertainties of the gig economy, more automated manufacturing, and even the role of restaurants in this new environment will take time to sort out.”

To solve the crisis, assuming treatment and a cure for the coronavirus COVID-19 pandemic is achieved, will require extraordinary planning and system reform.

We can no longer simply pursue the same old paradigm, as The New York Times Editorial Board recently put forth, that believes the world will be saved if fixed wages and benefits are increased to a level beyond the dreams of avarice of a century ago. The irony that the higher fixed wages go, the worse off workers become seems to escape them as the price level rises more than the wage increase, and workers get replaced by less expensive machinery and/or the controlling business owners shift production to low cost slave-wage labor countries.

The reason American workers have suffered a devastating loss of economic power over the past four decades, is two-fold: 1) As unions and workers demanded increases in wages and benefits for the same worker input, the controlling owners of corporations began to automate their production and in the process, they owned greater asset values; 2) they also sought to significantly lower the cost of labor and other cost factors, such as regulations and taxes, by shuttering manufactories in our homeland and investing in developing countries, such as Communist China and other slave-wage Asian countries, who welcomed the American investment, technology-sharing, and opportunity to develop their manufacturing capabilities.

Unfortunately, our political leaders over the past five decades have paved the way for an exodus of our manufacturing, led by the controlling owners of American corporations and industries, and their political allies, resulting in direct investment in the development and execution of manufacturing in slave-wage countries. Aided by years of massive tax cuts and incentives they built manufactories and offices around the world, shutting down manufactories and jobs in our homeland. This investment and exodus have enabled those countries to build their productive and technological capabilities, and in the case of Communist China become the world’s manufactory, while thousands of factories were shut down and millions of jobs were eliminated in the United States. Restoring manufacturing in the United States no doubt will prove a rough transition, as just in the past two decades since free trade was opened, China has dominated the production of goods previously manufactured in our homeland.

For the controlling owners of American corporations, it was cheaper to relocate production offshore, invest and manufacture goods offshore, and import back the products to the United States. Expanded free trade was supported with tax breaks to corporations offshoring production. Thus, production and importing back for American consumption was made even cheaper and thus more profitable still.

While intermediate supply chain and final goods exported from Communist China to the United States have been halted in some industries, we have yet to rebuild and expand our own homegrown manufacturing capabilities, and, as a result, we remain dependent on foreign supply chain and finished goods production. Not only are we still dependent on China, but even products in Japan’s and South Korea’s supply chains are essentially made in China and other parts of Asia, with materials and goods delivered to those countries, and then exported to the United States. The same situation is true for goods shipped to Mexico from Asian sources and then exported as final goods to the United States –– or from Asia to Europe, and then to the United States.

The actions that got the United States where we are today include the failure to take United Auto Workers Walter Reuther’s advice to keep wages where they are and help workers get their increases from the bottom line. Reuther warned that higher wages would destroy entire industries by lowering their competitiveness in international trade. Had we taken Reuther’s advice, businesses would not have set up shop in slave-wage countries like China.

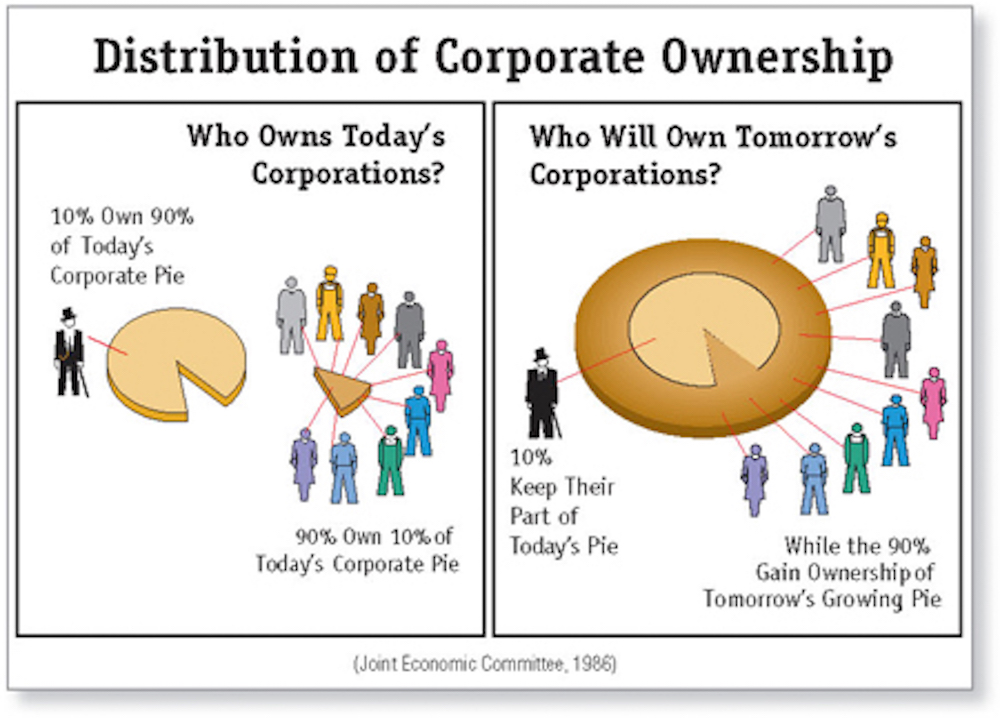

Why is broadening ownership so important? Ownership entails reaping the fruits of all contributions that one makes proportionately to the productive process, whether via the productive capital one owns or one’s labor, or both. A person’s labor is compensated either by wages or by a share of what the enterprise produces that is attributable to their labor contribution. It is important for ALL the employees to own shares of the companies that employ them to build a productivity culture throughout the organization. Owning thereby entitles workers to the rewards of their own labor as well as that produced by their proportionate share of the physical capital.

No one knows how much disruption our interconnected and service-oriented economy can endure, especially since the past few decades have seen a debilitating decline in and rapid exodus of our manufacturing capabilities. We should have instead been in constant retooling mode with restoration of our manufacturing capabilities and constant technological improvement through research and development. As a result, we no longer manufacture the clothing, appliances, electronics, furniture, cars, infrastructure materials, lifesaving medical equipment, medicines and all manner of supply chain production, necessary to live and consume in today’s world.

The net effect has been a significant drop in our homeland production and our growing dependency on foreign production. Regrettably, producer-corporations have unnecessarily extended their supply chains and finished goods manufacturing to all parts of the globe and invested in lower-cost foreign production in order to boost short-run profits and share prices for their owners. As a result, the American economy is exceedingly vulnerable to external shocks to our supply chains as the world’s supply chains are fixing to buckle and freeze-up, thereby causing production and incomes to fall abruptly. In turn, shrunken incomes and cash flows will collapse the edifice of non-productive debt and speculation that has been piled atop the American economy.

This crisis should finally make everybody realize that there needs to be self-sufficiency for EVERY individual and the country. We must decouple our manufacturing reliance on other countries, to the greatest extent possible, and fully develop our economic infrastructure to produce in our homeland.

This transformation to dependency on foreign manufacturing was largely ignored by the American public, who as consumers welcomed lower-priced non-American-made goods, ignoring or not realizing that globalization would destroy their only means to produce –– a job –– and thus their means to consume.

Still, during this time, economic output of the United States has almost tripled. And writers on the subject have attributed this to an increase in labor productivity. But the investment in productive capital (the non-human factor of production) does not “enhance” labor productivity (labor’s ability to produce economic goods). In fact, the opposite is true. It makes many forms of labor unnecessary as does the globalization of production to slave-wage labor countries.

Free-market forces no longer establish the “value” of labor. Instead, the price of labor is artificially elevated by government through minimum wage legislation, overtime laws, and collective bargaining legislation or by government employment and government subsidization of private employment solely to increase consumer income and create consumption demand.

The sole focus of government and the leadership that is supposed to represent our, the people’s best interests is job creation stimulated by investment in the businesses owned by the already wealthy capital ownership class.

Advocates for a job guarantee as the sole solution to when the economy contracts are promoting endless wage slavery, albeit to provide socially useful work

Writers on the subject consistently fail to recognize and address that in the United States, and for that matter, everywhere in the world, productive capital is increasingly the source of economic growth. Logically, if this is an undeniable fact, shouldn’t productive capital become the source of added property ownership incomes for all? If one simply postulates that if both labor and capital are independent factors of production, and if capital’s proportionate contributions are increasing relative to that of labor, then equality of opportunity and economic justice demands that the right to property (and access to the means of acquiring and possessing property) must in justice be extended to all. This is the logical approach to prevent costs and prices from rising due to inflated fixed wages and benefits. Yet, sadly, the editorial board of The New York Times, and for that matter, the American people and its leaders, still pretend to believe that labor is becoming more productive and couch all policy directions in the name of job creation and wage increases, while envying the wealthy capital asset ownership class. Americans ignore the necessity to broaden personal ownership of wealth-creating, income-producing capital asset portfolios simultaneously with the growth of the economy, and create consumption demand.

No matter how much labor is necessary or unnecessary in the economy, it is imperative that the issue of concentrated capital ownership is addressed, and policies are enacted to simultaneously create new capital owners of the corporations growing the economy, both established and viable start-ups,as the economy grows.

Why is it that educated people cannot see the weakness of the wage slave system? How is it that the vast majority of Americans virtually never learn about why the rich get so much richer every year while everyone else gets left behind?

There is no question that we need to get big money out of politics, which allows the wealthy to control policy-making to the benefit of their ownership interests. As well, we need to set social responsibilities for the controlling owners of corporations that regulate their operations. Political democracy can only be meaningful if supported by economic democracy. Benjamin Watkins Leigh and Daniel Webster understood this when they stated a simple fact: power follows property. “Property” will either seize power, or “power” will take over property. The real solution is to open up access to the opportunity and means for everyone to become capital owners.

We need to simultaneously ensure equal opportunity for EVERY child, woman, and man to acquire ownership stakes in the wealth-creating, income-producing productive assets as they are formed and our economy grows, not just focus only on job creation. This can be achieved without the requirement of holding a job or past saving to risk using insured, interest-free capital credit, solely repayable with the full pre-tax earnings of the investments. The loans would be insured using private capital credit insurance or public insurance. Government guarantees all sorts of things: loans, contracts. It’s not novel for the public sector to provide guarantees.

Citizen-Owned Federal Reserve

One feasible way to significantly broaden capital ownership simultaneously with the responsible growth of the economy is to lift ownership-concentrating Federal Reserve System credit barriers and other institutional barriers that have historically separated owners from non-owners and link tax and monetary reforms to the goal of expanded capital ownership. Removing barriers that inhibit or prevent ordinary people from purchasing capital that pays for itself out of its own future earnings is paramount as an actionable policy. This can be done under the existing legal powers of each of the 12 Federal Reserve regional banks, and will not add to the already unsustainable debt of the federal government or raise taxes on ordinary taxpayers.

We need to free the system of dependency on Wall Street and the accumulated savings and money power of the rich and super-rich who control Wall Street. The Federal Reserve System has stifled the growth of America’s productive capacity through its monetary policy by monetizing public-sector growth and mounting federal deficits and “Wall Street” bailouts; by favoring speculation over investment; by shortchanging the capital credit needs of entrepreneurs, inventors, farmers, and workers; by increasing the dependency with usurious consumer credit; and by perpetuating unjust capital credit and ownership barriers between rich Americans and those without savings.

The Federal Reserve Bank should be used to provide interest-free capital credit (including only transaction and risk premiums) and monetize each capital formation transaction, determined by the same expertise that determines it today — management and banks — that each transaction is viably feasible so that there is virtually no risk in the Federal Reserve. The first layer of risk would be taken by the commercial credit insurers, backed by a new government corporation –– the Capital Diffusion Reinsurance Corporation (CDRC) –– through which the loans would be guaranteed. The CDRC would reinsure any portion of any financing risk assessed as reasonable and insurable but not already insured by the commercial capital credit insurance underwriters. In establishing the CDRC, the federal government would not be undertaking a new responsibility but merely simplifying and rationalizing an existing one. This entity would fulfill the government’s responsibility for the health and prosperity of the American economy.

The Capital Diffusion Reinsurance Corporation would function similar to the Federal Housing Administration, generally known as “FHA”, which provides mortgage insurance on loans made by FHA-approved lenders throughout the United States and its territories. The FHA insures mortgages on single family and multifamily homes including manufactured homes. FHA borrowers pay for mortgage insurance, which protects the lender from a loss if the borrower defaults on the loan. While pay-downs on home mortgages require a separate source of income, capital credit for productive capital formation is self-liquidating, with the earnings from the investment the source of the pay-down.

The fact is money power rules. When money power is broadly distributed in the hands of the citizens, not the politicians or bankers, the people shall rule. Ensuring that money power is broadly distributed should be the primary role of the Federal Reserve.

The Federal Reserve Board is already empowered under Section 13 of the Federal Reserve Act to reform monetary policy to discourage non-productive uses of credit, to encourage accelerated rates of private sector growth, and to promote widespread individual access to productive credit as a fundamental right of citizenship. The Federal Reserve Board needs to re-activate its discount mechanism to encourage private sector growth linked to universal capital ownership opportunities for all Americans.

The Federal Reserve, which has been largely responsible for the powerlessness of most American citizens, should set an example for all the central banks in the world. Members of the Federal Reserve need to wake-up and implement Section 13 paragraph 2, which directs the Federal Reserve to create credit for local banks to make loans to finance economic growth. We should not destroy the Federal Reserve or make it a political extension of the Treasury Department, but instead reform it so that the American citizens in each of the 12 Federal Reserve Regions become the owners, who would regulate the monetization process. The result will be that money power will flow from the bottom up, not from the top down, not for consumer credit, not for credit that doesn’t pay for itself or non-productive uses of credit, but for credit for productive uses to expand the economy’s rate of socially responsible and environmentally enhanced growth.

By implementing Section 13 of the Federal Reserve Act the central bank can be used as a means to make every American a productive capital owner, serving as the only alternative to the two twin oligarchies of capitalism and socialism.

System Reform

As we conquer the COVID-19 virus and push forward, we will need to put into place a reformed monetary and tax system designed to facilitate building a future economy and society that provides equal opportunity for EVERY citizen to participate as owners of productive capital assets. Together we can achieve universal general affluence, based on our core values of fairness, respect, kindness, equal opportunity, courage, persistence, resilience, accountability and justice –– values that can unite us.

The bottom line is that American prosperity must be inclusive, with equal opportunity for EVERY citizen to gain ownership stakes in the corporations growing the economy and to share profits and productivity gains across the economic spectrum. We must include non-managerial and managerial workers, current shareholders, workers not employed in corporations and non-employed citizens –– of every age, race, color and ethnicity.

We must now reform the system and prevent those at the top of the income and wealth scale from exclusively benefiting from economic growth at the expense of the vast majority, and see to it that EVERY citizen, including all workers, enjoy the fruits of economic growth as we, following our triumphal containment of the virus, build an economy that can support general affluence for EVERY child, women and man.

One thing is certain, we have the opportunity to affect necessary system reform before the pandemic disruption has a permanent negative effect, and to embrace the development of tectonic shifts in the technologies of production to grow our economy responsibly and sustainably, and protect and enhance our environment so that EVERY child, woman and man can enjoy a healthy and prosperous future.

Economic stimuli in the moment must focus on emergency government spending and worker income restoration to stimulate investment and consumption. Once the pandemic ends, however, we must immediately shift to long-term systemic reform. The priority must be to create capital ownership estates for EVERY citizen. In the interim, planning for systemic reform and execution is essential and mandatory.

While policy makers and aware citizens know that unlocking the economy will be a difficult and painful process, no one knows exactly what the post-COVID-19 economy will look like.

The key issue in the post economic crisis will not be a lack of new money, but a lack of new owners of productive capital, resulting from a lack of a monetary system that universalizes equal opportunities for every person to access and acquire ownership stakes in the productive capabilities to be developed to meet future economic needs. Had stimulus packages in previous years been designed to create new owners along with new capital formation, our economy would have experienced sustainable and non-inflationary growth. More resources would have been available, and more people would have been economically secure and not dependent solely on jobs to deal with disasters such as the COVID-19 pandemic.

Collateralized by capital credit insurance, self-liquidating capital credit should, as a fundamental right, be made available on an equal basis to all citizens. This would turn today’s non-owners into economically independent owners of productive capital. Such credit would finance the purchase of new or existing productive assets needed by businesses. Future earnings on the shares would pay off the acquisition loans.

What’s needed is an immediate restoration of consumer household spending power and a protective floor under incomes that may soon also collapse should mass layoffs emerge once again in another two or three months.

In the immediate short term, strictly as an emergency measure, massive government debt will be required, which will add substantially to the national debt now exceeding over $26 trillion (or about $72,000 per citizen) and increasing. Such debt results when the government spends money created and regulated by the central bank that has nothing of value behind it other than the government’s promise to pay in the future via taxation. Those measures, however, should cease immediately after the crisis is over. Future taxes should be collected to repay the government’s increasing debt from deficit spending.

A JUST Third WAY Economic Personalization Response

If people were not surviving paycheck to paycheck, already making a livable wage and generating additional income through Capital Homesteading dividends from 24/7 automated production, they would be better equipped to survive shutdowns and self-isolations while the government figures out how to get them help.

What’s needed is an immediate restoration of consumer household spending power and a protective floor under incomes that may soon also collapse should mass layoffs emerge once again in another two or three months.

In the immediate short term, strictly as an emergency measure, massive government debt will be required, which will add substantially to the national debt now exceeding over $26 trillion (or about $72,000 per citizen) and increasing. This additional debt could amount to over $7 trillion. Such debt results when the government spends money created and regulated by the central bank that has nothing of value behind it other than the government’s promise to pay in the future via taxation. Those measures, however, should cease immediately after the crisis is over. Future taxes should be collected to repay the government’s increasing debt from deficit spending.

Where the new crisis money can be channeled to private sector businesses to produce emergency medical and other supplies needed during the pandemic, such money should flow as loans through financing mechanisms that create equal capital ownership opportunities for every employee in the companies producing the supplies. The government would serve as the guarantor of those loans, and as the customer that distributes the emergency goods where needed.

Capital Homestead Act

As a matter of national policy, immediately enact the Capital Homestead Act (aka Economic Democracy Act and Economic Empowerment Act) proposed by the Center for Economic and Social Justice (www.cesj.org). The act would establish citizen tax-sheltered Capital Homestead Accounts (CHAs) for each citizen (see http://www.cesj.org/learn/capital-homesteading/capital-homestead-act-a-plan-for-getting-ownership-income-and-power-to-every-citizen/).

The Act provides for the post-pandemic response to reform the system for inclusive growth and prosperity, broadening capital ownership simultaneously. The financial instruments and tools provided in the Act would empower EVERY citizen to transition from a non-owning wage or welfare slave, beholden to those who are owners or the government, into an economically independent owner of wealth-creating, income-generating productive capital.

To build a future economy, self-liquidating zero percent interest capital credit loans, collateralized by capital credit insurance, would be equally allocated, on an annual basis based on the projected capital needs of businesses, to EVERY citizen (children, women and men, from birth to death) exclusively for the purpose of investing in the new growth and transferred capital of the economy. These loans would cover all costs of purchasing voting, full-dividend payout shares of corporations and cooperatives that produce goods and services for potential national and global consumers.

The access to insured, self-liquidating zero percent interest capital credit loans would have to be truly universal to remove the stigma attached to means-tested programs such as food stamps. An equal amount of annual capital credit would go to everyone, whether they’re employed or not. No strings attached. No means test. No politicians demanding that you seek out even a menial job before getting the loans.

Each citizen’s capital acquisition loans would be wholly repayable with the full pre-tax stream of future profits earned on the shares, without any requirement to pledge past personal savings or reduce salaries, wages or benefits to invest.

The new monies would be used to invest in responsible and sustainable, environmentally sound growth projects and infrastructure, including alternative energy expansion and other climate crisis mitigation. These new development projects would hire workers in addition to creating new owners. This will be necessary since the current crisis will mean conventional private business investment will collapse across the board and such much needed investment will no longer be forthcoming from the private sector to revive the economy and create general affluence for EVERY citizen.

With the new monies, all manner of environmentally enhanced and sustainable projects can be planned and executed such as clean energy expansion, carbon pollution elimination, public transit development, robust infrastructure construction, smart grid expansion, green building, new “smart” cities, urban redevelopment, housing developments, homeland manufacturing capabilities, etc.

Immediate Response –– Capital Credit And Government Loan Guarantees

We need to use the powerful and proper function of commercial banks to create money by making loans and canceling money once loans are repaid. For this, commercial banks charge a one-time service fee (not interest) to cover administrative costs. Therefore, creating money can be entirely interest free (but not cost free). In addition to the principal to be repaid on interest-free capital credit loans to citizens, there would be a one-time premium to cover the risk of loan default as well as reasonable charges for the services of the Federal Reserve and commercial bank lenders.

Instead of printing trillions of dollars and giving it away, we need to make the money available as commercial loans with repayment guaranteed by the federal government.

In the immediate short term while the pandemic has the economy locked down, any corporation that receives an interest-free capital credit loan from a commercial bank “sold” to the Federal Reserve through the Discount Window with a federal government loan guarantee (loan default insurance via a Capital Diffusion Reinsurance Corporation or CDRC) would be required to issue full-dividend payout, voting shares in the amount of the proceeds of the loan and allocate the shares equally to each employee. The shares would be put into an escrow account until such time the capital credit loan is repaid. For the duration of the emergency, all debt service payments would be suspended.

Throughout the pandemic, the corporation benefiting from the federal government-backed grants, loans and loan guarantees would pay EVERY one of its employees an equal amount of emergency wage income sufficient to meet subsistence needs. These subsistence wages could not be used for acquiring capital. Payments for consumption needs should be in the form of grants that are passed through dollar for dollar to employees during the duration of the crisis to support purchase demand and enable the economy to keep functioning. The emergency capital credit loans would be used to finance broadly owned new productive capital investment to restart production and expand productive capacity.

Once the interest-free (but not cost free) working capital and new long-term capital loans are repaid with a reasonable capital cost recovery period, the money that was created to operate and purchase the capital and then repaid would be cancelled, avoiding both inflation and deflation. The capital itself would continue to produce wealth and generate consumption income for its new owners from ongoing full-dividend payouts from profits distributed as dividends tax deductible by the corporation but treated as regular income by the recipients. The capital would produce income indefinitely with proper maintenance and with restoration in the technical sense through research and development.

When normal operations resume, the corporation would cease emergency subsistence payments, with employees paid at market-determined rates, with any increases coming from profits instead of increasing fixed wages and benefits.

Under this proposal, when a corporation becomes profitable, pre-tax profits paid out as dividends (tax-deductible to the corporation) would be paid through tax-sheltered employee ownership accounts to the loan-issuing commercial bank, thus canceling the corporation’s indebtedness. As the loans are repaid, shares would be released from escrow and put into each employee’s individual Employee Capital Homestead Account (ECHA), a vehicle similar to today’s tax-sheltered Employee Stock Ownership Plan (ESOP) accounts. (ECHAs could later transition to full CHAs when the Capital Homestead Act for all citizens is passed and implemented.) Full-dividend payouts would be passed through (after reasonable deductions for bank administration costs) to each employee to use for consumption.

A politically practical alternative to creating a new legal vehicle (the ECHA) would be to channel government-guaranteed loans made through local banks to a company’s Employee Stock Ownership Plan Trust. ESOPs, which are tax-advantaged corporate finance vehicles, are already recognized under United States law, and thus would not require additional Congressional approval. ESOPs can be used by any company incorporated as a C-Corporation or an S-Corporation. For purposes of receiving government-guaranteed loans for working capital or long-term growth capital, ESOPs should be required to issue and allocate new, full-dividend, voting shares to all employees on an equal basis.

A politically practical alternative to creating a new legal vehicle (the ECHA) would be to channel government-guaranteed loans made through local banks to a company’s Employee Stock Ownership Plan Trust. ESOPs, which are tax-advantaged corporate finance vehicles, are already recognized under United States law, and thus would not require additional Congressional approval. ESOPs can be used by any company incorporated as a C-Corporation or an S-Corporation. For purposes of receiving government-guaranteed loans for working capital or long-term growth capital, ESOPs should be required to issue and allocate new, full-dividend, voting shares to all employees on an equal basis.

In a worst case scenario, in the event of loan default on the part of the corporation, the federal government making the emergency loan guarantee would repay the balance of the loan to the issuing commercial bank, in which case the loan is extinguished and the proceeds are used to redeem the commercial bank’s paper (promissory note) from the Federal Reserve.

Since 1985 in the United States, commercial bank loans for industry, commerce, and agriculture that have gone bad typically have been between 1 and 5 percent (https://www.federalreserve.gov/releases/chargeoff/delallsa.htm). Assuming that 5 percent of all government-insured commercial bank loans may default, a $2 trillion+ loan guarantee package would cost the government a lot less –– $100 billion or more depending on the total trillions of dollars guaranteed. The government can waive an insurance premium or, for example, charge a 1 percent premium, in which case the government would collect $20 billion and reduce the loss by that amount.

In immediate and future time frames, we must ensure that federal government grants and loans do not end up with corporations whose controlling owners would buy back their stock, in order to reduce the number of shares so the remaining shareholders can consolidate more ownership, and buy up the assets auctioned off by corporations that go out of business during the pandemic. Otherwise, without ownership-broadening stipulations tied to grants and loans, the result will be the ownership of our nation’s wealth will become even more concentrated than before the pandemic struck. Consequently, there will be more Americans poorer as poverty spreads while multi-millionaires and billionaires become wealthier.

Recovery Money Creation

As the economy recovers, all money backed by government debt should be gradually retired and replaced with money backed by private-sector productive capital assets.

After termination of emergency financing, EVERY citizen would be able to establish a Capital Homestead Account (CHA) that is legally advantaged to acquire new qualified full-dividend payout, voting shares of any corporation with fully insured, interest-free capital credit. A one-time premium to cover the risk of loan default as well as reasonable charges for the services of the central bank and bank lenders would be in addition to the principal to be repaid on capital credit loans to citizens. The corporations eligible would be both established and startups, and would use the money exclusively to fund viable projects to grow the economy. CHAs, as with the temporary ECHAs, would make the debt service payments with pre-tax dividends to Federal Reserve-backed commercial banks issuing the capital credit, and afterwards, upon liquidation, paid to citizen beneficiaries as regular taxable personal income.

As part of the normal money creation process, Federal Reserve policies should allow for covering reasonable and fair financing costs of the central bank and commercial banks providing interest-free capital credit loans annually and equally to EVERY citizen for the exclusive purpose of financing future capital expansion via corporations. If a corporation rejects citizen financing, they would not qualify for interest-free capital credit through the Federal Reserve/commercial banking system. Political and media pressure will help to persuade corporations to do the right thing and have ALL citizens share in our collective prosperity.

The grants or alternatively preferred government insured capital credit would finance the purchase of new or existing productive assets needed by businesses. Future earnings on the shares would pay off the grants or loans. Once the grants or loans are repaid, the money created to purchase the capital would be cancelled, avoiding both inflation and deflation. The capital itself would continue to be a source of wealth and generate consumption income for its new owners.

Capital Credit Insurance

A note about insurance: Once the economy has recovered, capital credit loans would be insured and guaranteed against loan default by private capital credit insurers, commercial risk insurers or a federal government reinsurance agency (á la the Federal Housing Administration mortgage insurance concept) –– the Capital Diffusion Reinsurance Corporation (CDRC) –– through which the loans would be guaranteed. The CDRC would reinsure any portion of any financing risk assessed as reasonable and insurable but not already insured by the commercial capital credit insurance underwriters. In establishing the CDRC, the federal government would not be undertaking a new responsibility but merely simplifying and rationalizing an existing one. This entity would fulfill the government’s responsibility for the health and prosperity of the American economy.

Such capital credit insurance would substitute for the security now demanded by lenders to cover the risk of non-payment, thus enabling the poor and others with no or few assets (the 99 percent) to overcome the collateralization barrier that excludes them from access to the means to finance their ownership of wealth-creating, income-generating productive capital. (A portion of their capital credit allotment will be used to cover the one-time cost of capital loan insurance and bank service charges.)

Before the loan is made, the lender, risk insurance company, and other entities will first determine the “feasibility” of each particular loan. (“Feasibility” means that the enterprise’s new capital investment is expected to generate enough profits to pay for itself within a reasonable capital cost recovery period. Such a feasibility analysis will judge the soundness of the enterprise that needs to purchase the new capital assets, including the quality of its management and workforce, its current and future markets, etc.)

Self-liquidating capital credit, collateralized by capital credit insurance, is critical for stimulating the economy’s recovery and responsible growth. Insured, interest-free capital credit should be made available annually on an equal basis to ALL citizens exclusively for investment, turning today’s non-owners into economically independent owners of productive capital simultaneously with the responsible growth of the economy. This credit would finance the purchase of new or existing productive capital assets needed by businesses. Future share earnings generated by the investments would pay off the acquisition loans –– in other words, past savings or reductions of current consumption income would not be necessary to finance capital formation.

Once the commercial bank loans are repaid, the money created to form the new productive capital would be cancelled, avoiding both inflation and deflation, and continue to generate consumption income for its new owners.

Every new productive capital increment added to the economy would generate future earnings to pay for its financing. Consequently, normal market forces would synchronize effective demand and supply for economic growth. This would continue as long as the new capital assets serve as an additional source of consumption income for today’s non-owning citizens, particularly the poor and others who do not have sufficient and secure incomes, thus reducing the need for government taxpayer redistribution and dependency on welfare, open and concealed. In this way, workers and other current non-owner citizens would help sustain economic growth and secure their own financial independence as they grow their wealth by becoming owners of the future increase in capital productiveness.

Further Economic Measures

Further economic measures will be needed to address the recession and recovery.

To meet the full costs of the government and start paying down its debt, a single tax rate should be imposed for all incomes from all sources above personal and family exemption levels so that the budget could be balanced automatically and even allow the government to pay off the growing unsustainable long-term national debt. The exemption should be sufficient to meet each citizen’s or family’s common domestic needs. The poor would pay the first dollar over their exemption levels as would the hedge fund operator and others now earning billions of dollars from capital gains, dividends, rents and other property incomes which under some tax proposals would be exempted from any taxes. Other personal taxes, such as payroll taxes, should be phased out. Remove all tax loopholes to eliminate corporate and personal tax avoidance, and business subsidies. Pay out of general revenues for all promises for Social Security, Medicare, government pensions, health, education, rent and subsistence vouchers for the poor until their new jobs and ownership accumulations provide new incomes to substitute for the taxpayer dollars to fill these needs.

To encourage full payout of corporate pre-tax earnings and finance new capital formation through the issuance and sale of new shares, dividends should be tax-deductible at the corporate level, enabling corporations to reduce their tax liability to zero. Dividends should be taxed as personal consumption incomes, except when used to pay for “qualified” shares (i.e., shares meeting required standards) held within each citizen’s tax-sheltered trust account. To pressure corporations to finance their growth, other than with retained earnings and corporation debt (neither of which creates any new owners), and pay out their full earnings as dividends to their actual owners, the corporate tax rate should be raised to at least 90 percent.

Leadership And Resolve

To overcome the COVID-19 coronavirus pandemic threatening our lives and our economy will require leadership, resolve, scientific knowledge, planning and resources. We must adopt laws promoting major reforms in monetary policy, central banking, tax and other laws for establishing a sustainable, resilient and just economy. Through a new visionary political and economic paradigm, we can build for EVERY person a more environmentally sound and sustainable economy that secures and enhances our personal futures, with preparedness to deal with future crises.

One sign of hope is the pandemic has turned millions of people into good neighbors with a sense of realization that we are all interdependent on each other. Hopefully that can translate to reforming the system so that ownership and power concentration can be reversed with EVERY child, woman, and man having the right to property and equal opportunity access to the means of acquiring and possessing property to enhance the economic security, safety, and well-being of ALL. This will ensure inclusive prosperity and economic justice as our nation progresses into the future in harmony with all the people on Earth.

Note: Some of the opinions expressed in this article are mine and not CESJ’s. Dawn Brohawn, Michael D. Greaney, and other CESJ colleagues contributed to this article.

Gary Reber is the founder and Executive Director of For Economic Justice (www.foreconomicjustice.org), a critic of economic policy and economic inequality, and an advocate and author for economic justice through broadened ownership of wealth-creating, income-producing physical productive capital. Mr. Reber is a board member of the Center for Economic and Social Justice (CESJ) and a founding member of the Coalition for Capital Homesteading. In 1967, Mr. Reber founded with binary economist, ESOP inventor, financial lawyer and universal citizen ownership theorist Louis O. Kelso, Agenda 2000 Incorporated to advocate policies and programs to broaden productive capital ownership in urban and economic development projects.