On September 17, 2013, Mark Gongloff writes in The Huffington Post:

No wonder so few Americans seem to think their economy is in recovery: They keep getting poorer. Unless they are rich, in which case they keep getting richer.

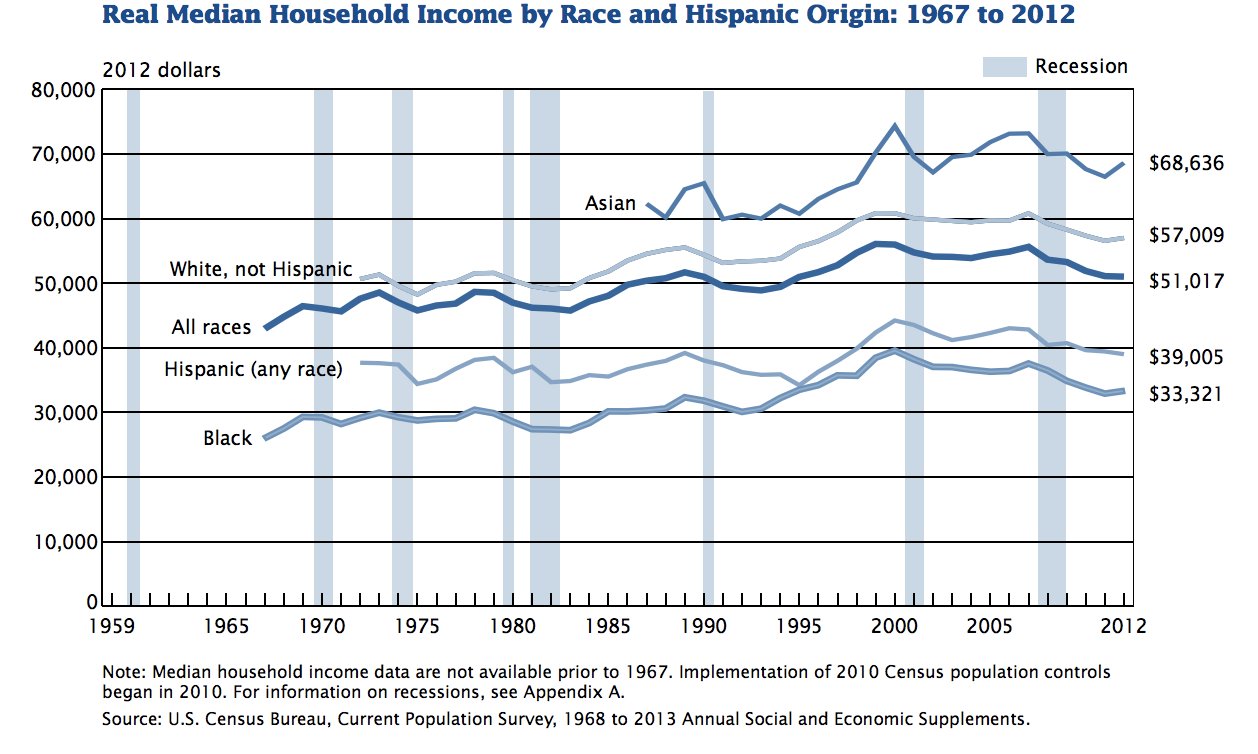

Median household income fell for the fifth straight year in 2012, the Census Bureaureported on Tuesday, to $51,017. That was the lowest annual income, adjusted for inflation, since 1995.

The typical American family’s income has fallen every year since 2007, the year the Great Recession began, for a cumulative decline of 8.3 percent. Median income is also down 9 percent from its record high of $56,080, set two recessions ago in 1999. (Story continues below depressing chart.)

While median income has fallen, the incomes of top earners have continued to rise, making income inequality worse. The Census Bureau’s measure of inequality, known as the “Gini index,” held steady at 0.477 in 2012, but at the record high set in 2011. A Gini index of 0 means perfect income equality, an index of 1 means one person would get all of the nation’s income. We’re slowly grinding our way towards 1.

The top 5 percent of all households earned 22.3 percent of all the nation’s income in 2012, matching its haul in 2011. The median income of households in the top 5 percent rose to $318,052 from $317,950 in 2011. The income of these highest-earning Americans has recovered completely from a dip during and after the recession, compared with the 8 percent decline for the median American household.

The racial differences in income are even starker: The median income for black households was $33,321 last year, less than half the median income for Asian households. The current federal poverty threshold for a family of four is $23,550.

These numbers help explain why, even though the Great Recession officially ended in June 2009, and even as President Barack Obama touts “progress” in the economy,one-third of Americans think we are still in a recession or a depression, according to a recent survey.

For many of them, the recovery has been worse than the recession.

The reality is that middle class wealth, for the most part, is the value of their primary residences. On average their retirement plans, for those who have one, only have an average of $30,000. The middle class is the engine of consumer spending, and as a result have spent (with directly earned monies and consumer debt) itself virtually into oblivion with increasing indebtedness and income security. Those whose job earnings have enabled them to save, beyond expending income to pay necessary day-to-day and month-to-month living costs, have faired a bit better. But even so, though millions of Americans own diluted stock value through the “stock market exchanges,” purchased with their earnings as labor workers, their stock holdings are relatively miniscule, as are their dividend payments compared to the top 10 percent of capital owners. On the other hand, the rich are rich because they own wealth-creating, income-generating productive capital assets which earn them dividends, rent, and interest income. Thus their income gains are due to equity market valuations and major business ownershipt.

This difference or inequality is a matter of OWNING productive capital assets versus NOT OWNING and solely dependent on a job for income. As tectonic shifts in the technologies of production will continue to transpire, jobs will further be destroyed (which increases the number of people seeking employment) and the worth of labor devalued, as well as by globalization, which shifts employment to other countries where labor is less costly as well as regulations and controls.

Conventional economists continue to confuse the incomes that the wealthy rich class earn with the incomes earned from labor. What needs to be STRESSED is that the reason the rich are rich is because their earnings are generated by their ownership of wealth-creating, income-generating productive capital assets––not a job! Labor workers ONLY have a job (and increasingly less opportunity for good-paying jobs) as their source of income. And if they are creditworthy they will have managed to finance and pay for the purchase of a primary residence, which at the end of 30 or so years is the asset of their lifetime. But they dare not sell this asset (because they always need a roof over their heads) unless they can re-purchase another residence that meets their housing needs at less cost and benefit financially from a capital gain earning. But most Americans never even achieve this small degree of financial security and continuously live financially insecure their entire life.

This deplorable situation will worsen as long as we as a nation fails to address the REAL problem at the root of income inequality and poverty––CONCENTRATED OWNERSHIP of wealth-creating, income-generating productive capital. And to advocate for solutions that systematically broaden private sector individual ownership of the formation of FUTURE productive capital investment to empower EVERY American to accumulate over time a viable capital trust (super-IRA) portfolio of stock in diversified companies and reap the full earnings payout of corporate earnings as dividend income to support their livelihood and retirement. Such economic policy will build REAL financial security and wealth assets that generate annual incomes.

What is needed is leadership and government policies that result in the enrichment of EVERY citizen, not just those who already OWN America. How to achieve this solution is outlined in “Financing Economic Growth With ‘FUTURE SAVINGS’: Solutions To Protect America From Economic Decline” at NationOfChange.org http://www.nationofchange.org/financing-future-economic-growth-future-savings-solutions-protect-america-economic-decline-137450624 and “The Income Solution To Slow Private Sector Job Growth” at http://www.nationofchange.org/income-solution-slow-private-sector-job-growth-1378041490.