On July 19, 2019, Paul Brandus writes on Market Watch:

The coming ‘tsunami of poverty’ for retirees — and what to do about it

ReutersSome sobering facts for older Americans.

First the good news: As you know, the stock market has surged for more than a decade. Since the recession low of March 9, 2009, the S&P 500 SPX, -0.62% has rocketed from a devilish 666 to over 3,000 today. That’s a gain of 350% in 10 years. Talk about building wealth.

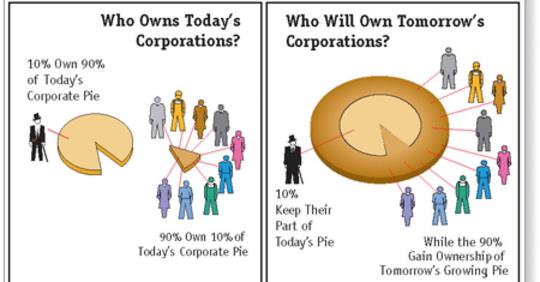

Now the bad news: This incredible period of wealth creation has bypassed tens of millions of older Americans — perhaps including you. That’s because — get this — the wealthiest 10% of households own 84% of all stocks—and that includes pension plans, 401(k) accounts and individual retirement accounts (IRAs) as well as trust funds, mutual funds and college savings programs like 529 plans. That means 90% of American households own the remaining 16% of all stock.

These sobering stats come courtesy of Edward N. Wolff, an economist at New York University, who tells the New York Times “For the vast majority of Americans, fluctuations in the stock market have relatively little effect on their wealth, or well-being, for that matter.”

And it’s not like older Americans had a little bit saved a decade ago and made some gains — maybe a few hundred or a few thousand dollars — over the past 10 years, but not enough to make much of a difference in their lives. Many have — literally — nothing. According to the U.S. Government Accountability Office (GAO), nearly half of Americans aged 55 or older have nothing set aside in a 401(k) or other individual account. Nothing. The adage that the rich get richer and the poor — well, you know the rest — certainly seems true.

Of course individual savings are, or should be, only one source of income for retirees. Pensions and Social Security are the others. But three-fifths of such households — again headed by someone 55 or older — do not have a traditional pension. This leaves Social Security, which, as we’ve explained many times before, has troubles of its own.

And remember: Social Security is only supposed to be a supplement for pensions and personal savings — yet more than half of senior households rely on it for at least half their income. Up to a quarter of them rely in it for 90% of their income — a near total dependency.

Adding to senior woes is growing debt. In 2010, says the National Council on Aging, 51.9% of households headed by an adult aged 65 or older had some debt. Just six years later that percentage had jumped to 60%. The median level of that debt in 2016 was $31,300 (median means half have more debt than that half have less).

Counterpoint: Fears of a retirement crisis are overblown — these numbers prove it

All of this helps explain how utterly unprepared tens of millions of Americans are for retirement, and why many in fact, will never retire at all — at least not in the way they probably envisioned when they were younger. I call this, perhaps with a bit of hyperbole, a “tsunami of poverty and deprivation” that is fast approaching and seems unstoppable. A 350% stock market gain offered the opportunity to flee to higher ground, but most missed out.

“The problem now is that many years have passed, and that means less time to make up for lost ground,” says Reginald Nosegbe, chief executive officer of Valspresso, a fintech and investment strategy firm based in Reston, Va. He warns that older people trying to make up for retirement shortfalls may move into riskier assets — at a time in their lives when they’re supposed to be dialing back risk. That’s if they even have assets to invest in the first place, of course.

“It’s always a good time to save and to invest,” Nosegbe says. “But be prudent about it. No matter who you are, talking things ever with a financial adviser is always a good idea.”

If this is you — you’re an older worker with little to nothing saved — there’s no sugar coating it: you’re in a tough spot. But there are things to do that can help. At the risk of sounding presumptuous, here are five big things for you to consider:

• Pay down your debts. If you are carrying credit card debt, pay as much as you can toward the card with the highest rate — and consider rolling it over onto a lower card if the numbers make sense. Avoid new debt like the plague.

• Visit a financial adviser and see what retirement vehicles you can open with just a minimal investment.

• Consider moving to a smaller home. Monthly payments, upkeep and insurance may be cheaper.

• Cars are money pits: payments, maintenance, gas, tolls — not to mention the stress of rush hour traffic. Avoid all that, if you can, and take mass transit — you can save a small fortune.

• Exercise and eat well. Keeping fit will reduce medical bills as you age. You’ll save an enormous amount of money.

Gary Reber Comments:

This is a an article, as well as the references included, that calls attention to the serious condition of advancing poverty among the masses of Americans, particularly our senior citizens, who are increasingly struggling to survive economically.

For the majority of senior citizens, Social Security is their ONLY means to live. While Social Security payouts are going up 2.8 percent in 2019, the biggest rise in seven years., that only translates into an average benefit of $1,461 a month, up $39.

The increase is tied to inflation, meaning that higher payouts will simply enable senior citizens to keep up with the rising cost of living, not better their standard of living.

A study by the Schwartz Center for Economic Policy Analysis at the New School finds that about 40% of middle-class Americans will live close to or in poverty by the time they reach age 65.

More people retire at 62 than any other age. Age 62 is the earliest age they can tap into Social Security. But remember Social Security is tied to one’s work history, so the payout is not equal to all persons.

If you’re an average, single middle income earner and retire at 62 in 2019, you’ll get $17,532 from Social Security next year. While that’s well above the $12,060 the federal government considers the official poverty level for a single person, in reality, it remains at the level of economic deprivation.

What are the other sources of retirement income? Pensions and personal savings would supplement Social Security, that is if people had them. But again the reality is that 91 percent of workers in their 50s don’t have a pension, and 46 percent don’t participate in a retirement plan where they are employed — not an IRA or 401(k), absolutely nothing.

This is a huge problem. Social Security was never meant to be a principal source of income — but merely a supplement to pensions and personal savings.

As is noted in the article, statistically, stock market wealth is held by a relatively small number of the most affluent. In reality, most Americans don’t have any stocks to their name. In fact, many Americans don’t even have any savings to their name. Pew Research found that 53 percent of Americans own no stock at all, nor have any retirement accounts, and out of the 47 percent who do, the richest 5 percent own two-thirds of that stock. And only 10 percent of Americans have pensions, so stock market gains or losses don’t affect the incomes of most retirees.

Though millions of Americans own diluted stock value through the “stock market exchanges,” purchased with their earnings as labor workers, their stock holdings are relatively minuscule, as are their dividend payments, if any, compared to the top 10 percent of capital asset owners.

What historically empowered America’s original capital owners was conventional savings-based finance and the pledging or mortgaging of assets, with access to further ownership of new productive capital available only to those who were already well capitalized. As has been the case, credit to purchase capital is made available by financial institutions ONLY to people who already own capital and other forms of equity, such as the equity in their home, business and/or capital assets, that can be pledged as loan security — those who meet the universal requirement for collateral. Lenders will only extend credit to people who already have assets. Thus, the rich are made ever richer through their continuous accumulation of capital asset ownership, while the poor (people without a viable capital estate) remain poor and dependent on their labor to produce income. Thus, the system is restrictive and capital ownership is clinically denied to those who need it.

At the root of the problem is the “savings” requirement barrier, and why we need to free economic growth from the slavery of savings.

While the system is based on past savings and thus a denial of consumption, personal savings is not the norm among the vast majority of American households who must spend virtually every earned dollar on living expenses. While increasingly individuals are finding it necessary to continue working in retirement to supplement their income, most older Americans discontinue full-time career work and struggle to meet obligations with minimum-pay part- and full-time jobs. A proportion of retirees also receive income from welfare programs, such as Supplemental Security Income and other life-support services funded through tax extraction and government debt.

Presently, the United States continues to benefit from never-ending technological innovation and invention. This is exponentially generating tectonic shifts in the technologies of production –– the effect of which destroys jobs and devalues the worth of labor’s contribution to the production of goods, products and services. Thus, as the non-human factor of production becomes increasingly more productive, there will continue to be less employment opportunities as long as the economy does not significantly expand, especially with respect to affluent-level wage and salary income opportunities.

The author of the article offers no concrete solutions for reversing the downward slide to poverty that is occurring or how to create an economy that can support general affluence for EVERY citizen.

Amazingly, as a nation we continue to not address this reality or to understand that there are two independent factors of production –– human labor and non-human productive capital that creates wealth and generates income to those who own it. Individuals own capital assets (typically through stock ownership in corporations) such as productive land, structures, infrastructure, tools, machines, robotics, artificial intelligence, computer processing, and certain intangibles that have the characteristics of property. Just as one owns his or her labor used as a source of personal income, capital owners are entitled to the wealth and income their capital produces. Thus, fundamentally, economic value is created through human and non-human contributions.

Because productive capital is increasingly the source of the world’s economic growth, shouldn’t we be asking the question why is not productive capital the source of added property ownership incomes for all? Why are we not addressing how the system facilitates greed capitalism and envy while concentrating productive capital ownership among the 1 to 10 percent of the population? One would think that a reasonable and logical conclusion would be to consider this postulation: if both labor and productive capital are independent factors of production, and if productive capital’s proportionate contributions are increasing relative to that of labor, then shouldn’t equality of opportunity and economic justice demand that the right to property (and access to the means of acquiring and possessing property) must in justice be extended to all?

What is needed is for the system to facilitate spreading the ownership of productive capital more broadly as the economy grows with full payout of dividend earnings, without taking anything away from the 1 to 10 percent who now own 50 to 90 percent of the corporate productive capital wealth assets (paying their full share of taxes while they are alive and spreading their wealth out to others at death). In doing so, the ownership pie would desirably get much bigger and their percentage of the total ownership would decrease, as ownership gets broader and broader. This would benefit the traditionally disenfranchised poor and working and middle class, who are propertyless in terms of owning productive capital assets. It would also result is tremendous economic growth, which would benefit everyone including the already wealthy ownership class, and create opportunities for real jobs, not make-work as an expanded economy is built that can support general affluence for EVERY citizen. Thus, as productive capital income is distributed more broadly and the demand for products and services is distributed more broadly from the earnings of capital, the result would be the sustentation of consumer demand, which will promote responsible and environmentally protective and enhanced economic growth. That also means that over time, EVERY man, woman and child could accumulate a diversified portfolio of wealth-creating, income-generating productive capital assets to provide economic security in retirement and not be dependent on having to work during retirement or rely on government-assisted welfare.

One might ask how we failed to grasp the significance of productive capital’s input and the necessity for broad private sector individual ownership? Unfortunately, ever since the 1946 passage of the Full Employment Act, economists and politicians formulating national economic policy have beguiled us into believing that economic power is democratically distributed if we have full employment –– thus the political focus on job creation and redistribution of wealth rather than on full production and broader productive capital ownership accumulation. This is manifested in the belief that labor work is the ONLY way to participate in production and earn income. Yet, the wealthy ownership class knows that this notion is idiotic.

One should ask what form would the structural reforms take. At birth, a Capital Homestead Account or “CHA” (a super-IRA or asset tax-shelter for citizens) would be established, in which the accumulation of wealth-creating, income-producing capital assets would be deposited into an asset growth portfolio. Employment in this new enlightened age would start at the time one enters the economic world as a labor worker, to become increasingly a productive capital owner, always expanding one’s capital asset portfolio, and at some point to retire as a labor worker and continue to participate in production and to earn income as a productive capital asset owner until the day you die.

At death, as a substitute for inheritance and gift taxes, a transfer tax would be imposed on the recipients whose asset holdings exceeded $1 million. This would encourage those owning concentrations of productive capital assets (effectively the 1 to 10 percent) to spread out their monopoly-sized estates to all members of their family, friends, servants and workers who helped create their fortunes, teachers, health workers, police, other public servants, military veterans, artists, the poor and the disabled.

Other stipulations for the structural reform would entail structuring a more just and simple tax system. The tax rate would be a single rate for all incomes from all sources above defined personal exemption levels so that the budget could be balanced automatically and even allow the government to pay off the growing unsustainable long-term debt. For example, a family of four would be provided an exemption of $100,000 to meet their ordinary living needs. The poor would pay the first dollar over their exemption levels as would the hedge fund operator and others now earning billions of dollars from capital gains, dividends, interest, rents and other property incomes. This would include the elimination of all tax loopholes and subsidies.

There would be tax policy to incentivize corporations to pay out all profits to their owners as taxable personal incomes to avoid paying stiff corporate income taxes and to finance their growth by issuing new full-dividend payout shares for broad-based individualized employee and citizen ownership with full-voting rights.

The payroll tax on workers and their employers would be eliminated, but all promises for Social Security, Medicare, Medicare, government pensions, health, education, rent and subsistence vouchers for the poor would be paid out of general revenues until their new jobs and ownership accumulations provide new incomes to substitute for the taxpayer dollars to fill these needs.

The structural reform policies would direct the Federal Reserve to create an asset-backed currency that could enable every child, woman, and man to establish a Capital Homestead Account at their local bank to acquire a growing and diversified dividend-bearing stock portfolio to supplement their incomes from work and all other sources of income. The CHA would process an equal, annual allocation of productive credit to EVERY citizen exclusively for purchasing full-dividend payout shares in companies needing funds for growing the economy and private sector jobs for local, national and global markets. The shares would be purchased on credit wholly backed by projected “future savings” in the form of new productive capital assets as well as the future marketable products and services produced by the newly added technology, renewable energy systems, plant, rentable space and infrastructure added to the economy. Risk of default on each stock acquisition loan would be covered by private sector capital credit risk insurance and reinsurance, but would not require citizens to reduce their funds for consumption to purchase shares.

The end result would be that citizens would become empowered as owners to meet their own consumption needs and government would become more dependent on economically independent citizens, thus reversing current global trends where all citizens will eventually become dependent for their economic well-being on our only legitimate monopoly –– the State –– and whatever elite controls the coercive powers of government to extract taxes, incur national debt and redistribute earnings from the productive sector.

For an in-depth overview of solutions, see my article “Economic Democracy And Binary Economics: Solutions For A Troubled Nation and Economy” at http://www.foreconomicjustice.org/?p=11

Support Monetary Justice at http://capitalhomestead.org/page/monetary-justice.

Support the enactment of the proposed Capital Homestead Act (aka Economic Democracy Act and Economic Empowerment Act) at http://www.cesj.org/learn/capital-homesteading/, http://www.cesj.org/learn/capital-homesteading/capital-homestead-act-a-plan-for-getting-ownership-income-and-power-to-every-citizen/, http://www.cesj.org/learn/capital-homesteading/capital-homestead-act-summary/ and http://www.cesj.org/learn/capital-homesteading/ch-vehicles/. And The Capital Homestead Act brochure, pdf print version at http://www.cesj.org/wp-content/uploads/2014/11/C-CHAflyer_1018101.pdf and Capital Homestead Accounts (CHAs) at http://www.cesj.org/learn/capital-homesteading/ch-vehicles/capital-homestead-accounts-chas/