On June 10, 2016, David Stockman writes on Contra Corner:

There is a deep irony embedded in the Fed’s savage assault on savers and its delusional doctrine of interest rate repression. While this actually results in monumental windfalls to speculators and the one percent, it’s all justified in the name of boosting the labor market and the wage bill.

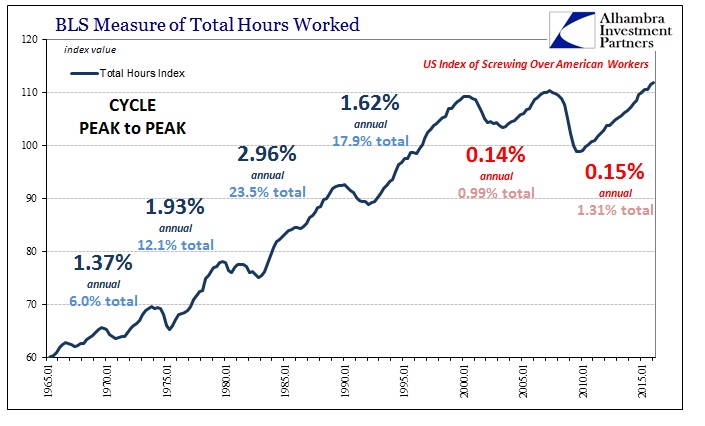

So the chart in Jeff Snider’s nearby post is especially salient. It shows that all this money printing has been for naught. Notwithstanding the 9X eruption of the Fed’s balance sheet from $500 billion at the turn of the century to $4.5 trillion today, growth in the most basic measure of labor input—-total hours worked——has come to a grinding halt.

Compared to labor hours growth of nearly 3% annualized during the Reagan expansion of the 1980s and nearly 2% during the start-and-stop stagflationary economy of the 1970s, labor hours growth over the two boom-and-bust cycles since the Fed went full frontal on money printing in December 2000 has averaged just 0.15% per annum.

Stated in aggregate terms, during the 10-year expansion between 1980 and 1990, labor hours employed in the US economy grew by 23.5%. By contrast, during the last 15 years combined, labor hours employed have risen by only2.3%.

Needless to say, this dismal outcome is not for want of potential labor supply. At the turn of the century, the civilian population aged 16 to 65 years was 177 million. That number has since grown to 205 million, meaning that the potential labor pool grew by 16% or nearly 7X faster than hours employed.

These figures also stick a fork in the Fed’s blind fixation on the U-3 unemployment rate and the nonfarm payroll numbers. Both are a relic of a half-century ago world of mines, factories, warehouses and retail shops based on a 40+ hour workweek on a year round basis.

By contrast, in today’s world of flexible just-in-time production, hours-based labor scheduling and gig-based employment patterns, there is really no such standardized labor unit as a “job”.

Likewise, the BLS conventions for counting as “employed” anyone on a payroll for even a few hours per week, and omitting from the labor force denominator tens of millions of potential workers not actively looking for jobs at the moment of the surveys, mean that its headline series are essentially noise.

Most certainly they do not validly measure economic “slack” in the labor force and therefore the degree to which the Keynesian bathtub of “potential GDP” is less than filled to the brim.

The silliness of the Fed’s targets is underscored by the graph below, which shows that the nonfarm economy is now employing only 15 billion more labor hours than it did in the year 2000. By contrast, assuming a standard work year of 2000 hours, the 28 million increase of the population 16-65 years old theoretically was capable of producing 56 billion more labor hours.

So only 27% of those potential hours were actually absorbed by the nonfarm economy.

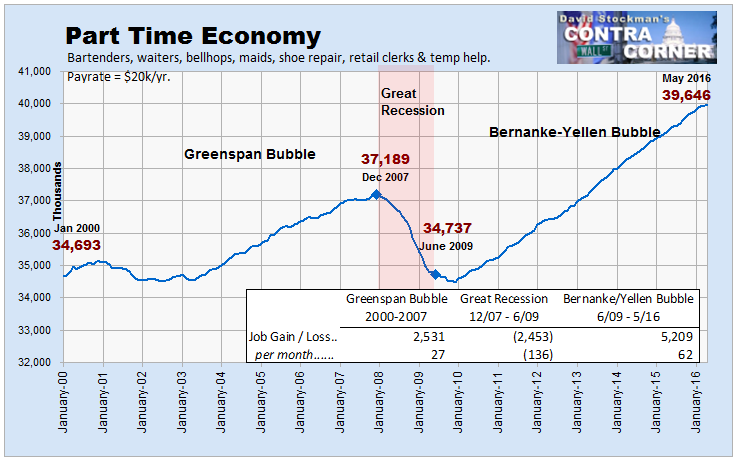

Likewise, as the jobs mix in the payroll report has shifted increasingly to what we have called the Part-Time economy of jobs in bars, restaurants, hotels, recreational venues, retail stores, temp agencies and household services, it has become self evident that the job count of 40 million workers in these categories has nothing to do with economic “slack” in the work force.

That’s because “jobs” in these categories average only about 27 hours per week of paid employment. On an annualized basis that’s a 1400 hour work year, meaning the Part-Time Economy depicted below generates about 56 billion labor hours annually. Yet a standard work year for these workers would amount to 80 billion labor hours.

The point is that without any change in the BLS headline numbers with respect to the U-3 unemployment rate or any increase in the nonfarm payroll total, there is 24 billion unutilized labor hours in this segment alone that could supplied to the US economy.

Now that’s “slack” and then some. It is virtually inconceivable that the tens of millions of hand-to-mouth workers in these jobs would not take an additional 5 hour or even 10 hours per week if offered at current wage rates. And that represents 10 to 20 billion additional labor hours.

So the headcount-based metrics of the BLS are useless for establishing monetary policy targets; and the occupants of the Eccles Building couldn’t do much about achieving a better, more modern hours-based target, anyway.

That’s because the true labor utilization rate and the actual amount of “slack” in the US economy is due to dozens of structural factors that the Fed has no ability to impact. Many of these are supply-side factors such as the doubling of the disability rolls during that period and the explosion of student loans and grants, which took billions of potential labor hours out of the economy.

Needless to say, these forces had nothing to do with that imaginary ether called “aggregate demand” by the Keynesians, nor could they be reversed by ultra-low interest rates.

At the same time, the off-shoring of manufacturing labor due to the China Price and back office service labor due to the India Price did reduce the demand for domestic labor by tens of billions of hours. But that was due to high US costs and labor rates, not high interest rates or anything else the Fed could impact.

Likewise, the decision of some spouses to work in the unmonetized economy rearing children and maintaining households is a function of culture and demographics, not interest rates. And it varies over time in ways that the central bank cannot anticipate, measure or impact.

In all, less than 60% of the 410 billion potentially available labor hours among the 16-65 year old population is employed in the monetary economy. And when you adjust for more than 14 billion hours supplied by the over 65 populations, which is included in the graph above, only 56% of available labor hours among the working age population are employed.

The point is that whether the hours based “employment rate” of the non-retired adult population should be 50% or 70% rather than the current 56% level is dependent on a plentitude of factors which totally overwhelm monetary policy.

For instance, shifting the current $1 trillion of annual payroll tax levies to a consumption tax would bring billions of additional labor hours into the US economy by changing the incentives of employers and employees alike.

By sharply reducing employment costs in sectors which compete with off-shored goods and services, it would increase the demand for domestic labor hours; and on the supply side it would improve the trade-off between work and welfare for low wages workers.

By the same token, on the margin, the current trend toward sharp increases in state and city minimum wages is reducing the demand for labor hours, and accelerating the substitution of automation and robots for low wage labor.

At the end of the day, there is no accurate way to measure full employment in an hours based economy, nor is it an especially appropriate target for public policy.

In fact, the labor hours utilization rate is an outcome. It is the happenstance result of the unfathomable interactions of taxes, welfare, trade, economic regulation, cultural preferences, demographics and the underlying efficiency and entrepreneurial dynamics (or lack thereof) of the market economy.

Even then, the Fed’s claim that the Humphrey-Hawkins Act makes them do it is nonsense. The statute is purely aspirational and content free on the matter of “maximum employment”.

The fact that the Fed even bothers with a U-3 target in the range of 5% is purely ritualistic and vestigial. It is self-evidently meaningless as a measure of economic “slack” in today’s globalized and sliced and diced labor markets. And the matter of whether the instruments of the state should be used to encourage citizens to study or travel rather than work, or to take disability payments rather than supply productive labor, is a matter for Congress to decide, not our unelected monetary politburo.

Forget JM Keynes, Paul Samuelson and James Tobin. The fact that the U-3 unemployment rate was in fashion among the Keynesian economists of the day when Humphrey-Hawkins was enacted in 1977 is little more than a historical curiosity.

That their primitive and outmoded economic model supplied the narrative and authority for the Act’s so-called “dual mandate” simply proves a variation of Keynes’ famous observation. Namely, that the purportedly practical men and women who run the Fed “are merely slaves of some defunct economist”.

In fact, today’s Fed could easily jettison its mechanical, misleading and obsolete U-3 based unemployment target and most of the other jobs series of the BLS. It could even be truthful and admit that 95% of what drives the real labor metric——-the labor hours utilization rate——— is beyond the reach of monetary policy; and that much of what forms how much “slack” we have—-like early retirement, late retirement, homemaking and child care, college enrollment—— is not even the business of government.

Needless to say, that would essentially put it out of the macroeconic management business and dramatically reduce its reason for massive intrusion on the money and capital markets. Indeed, it would imply that its real job is to provide back-up liquidity to the banking system at a penalty spread above market determined interest rates and yield curves.

It just so happens that this was the original mission assigned to it by its author, Congressman Carter Glass, in the 1913 Act which created the Fed.

The Fed that Carter Glass envisioned only needed to recognize good collateral when posted by member banks seeking liquidity loans. It did not need to know what “full employment” is in the context of 410 billion potential labor hours or whether there was too much or too little “slack” or whether the bathtub of potential GDP was filled to the brim or not.